Transforming Risk Management for Lenders: A Smarter Approach to DACAs with Arc

For non-bank lenders, managing risk within their portfolio companies is crucial. Deposit Account Control Agreements (DACAs) have traditionally been a key tool in this process. However, setting up DACAs with traditional banks can be slow, costly, and often inadequate. Arc is changing this landscape by streamlining the DACA process and providing real-time risk management tools, giving both lenders and borrowers greater control and efficiency.

The Hidden Challenges of DACAs

Despite their intended benefits, traditional DACAs often present several challenges:

- Slow Process: Banks can take weeks to set up a DACA account or respond to activation requests, delaying borrowers' access to capital and reducing security for lenders.

- High Costs: Banks typically charge borrowers a one-time DACA setup fee and monthly maintenance fees, ranging from a few hundred to thousands of dollars, adding financial burden to borrowers.

- Reactive Protection: DACAs often serve as an emergency safety net after a problem has occurred. Lenders prefer real-time liquidity monitoring for more proactive risk management.

- Delayed and Cumbersome Liquidity Monitoring: Lenders often rely on borrowers to send monthly bank statements, leading to delayed insights. Even if borrowers provide lenders with login access to their online banking portals, managing multiple logins and manually tracking balances can be operationally cumbersome.

Arc: A Modern Solution for Lenders and Borrowers

Arc transforms the DACA experience by offering a digital-first cash management platform that addresses the challenges faced by both lenders and borrowers.

Digital-first cash management trusted by thousands of businesses. Arc's cash management platform, developed in partnership with Stripe and with funds held at Fifth Third Bank, provides a modern cash management experience tailored for today's businesses. Funds are securely held with FDIC-insured institutions, offering peace of mind to both lenders and borrowers.

Responsive and cost-effective. Arc streamlines the process of opening cash management accounts and setting up control agreements. The self-serve onboarding process takes less than 10 minutes, and once an account is approved, control agreements can be established promptly, expediting deal execution and reducing administrative burdens. Arc does not charge additional fees for control agreement setup or maintenance, alleviating financial strain on borrowers.

Flexible permission settings to meet your needs. Arc provides customizable permission settings to fit different control agreement arrangements. For a Springing control agreement account, borrowers can grant lenders read-only access to their Arc accounts, enabling lenders to monitor account activity without interfering with daily operations. For a Blocked control agreement (BACA) account, borrowers can assign lenders admin access, allowing them to set up withdrawal approval rules. This ensures lenders maintain control over fund movements, offering a more proactive approach to risk management.

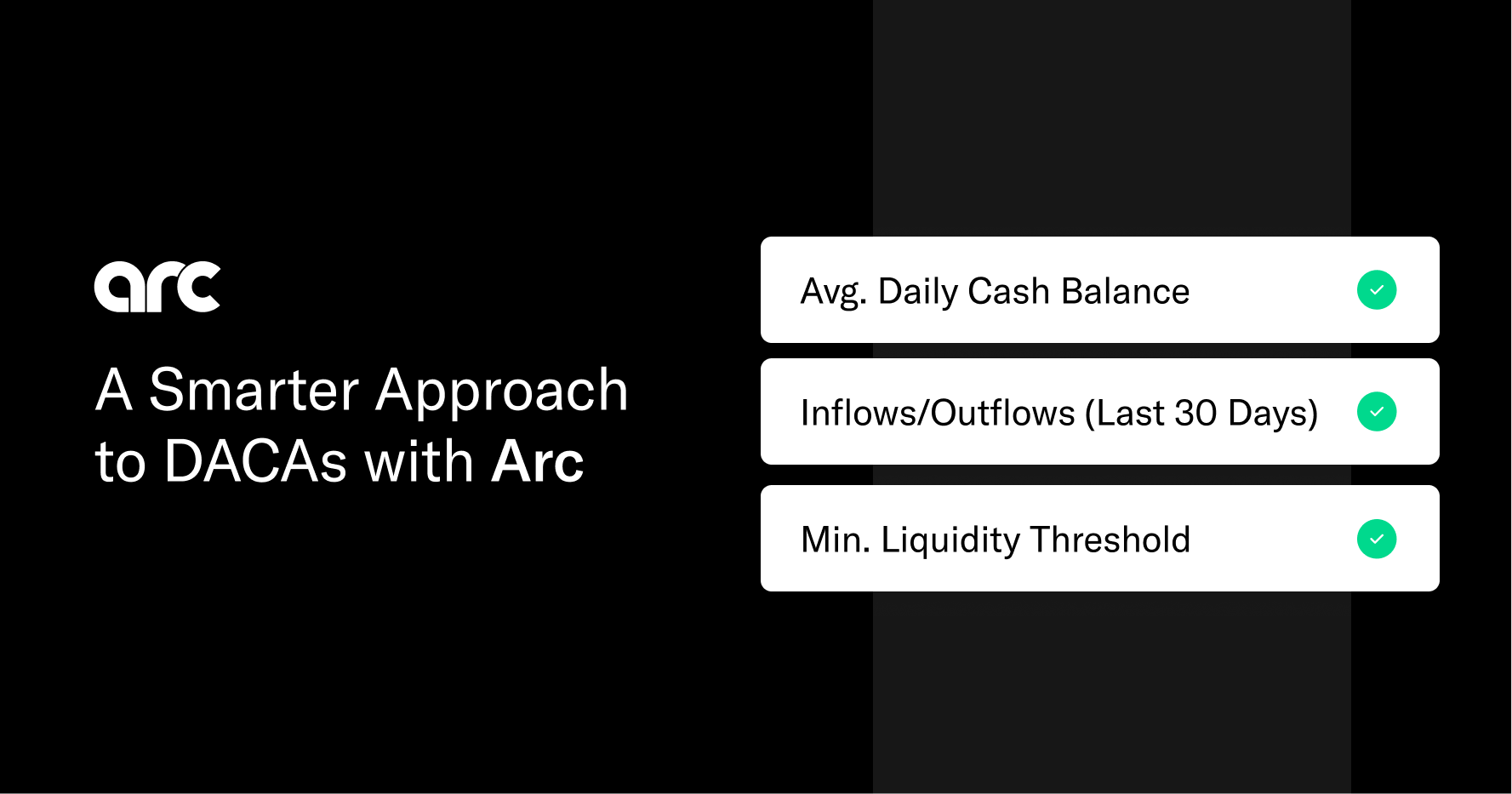

Centralized portfolio cash dashboard. Lenders can view all their portfolio companies that have set up control agreement accounts with Arc in a consolidated dashboard. Easily access current balances, total inflows and outflows in the past 1, 7, or 30 days. This centralized approach eliminates the need to juggle multiple logins and provides a clear overview of portfolio liquidity.

Intelligent and proactive monitoring. Arc's proactive monitoring system notifies lenders and borrowers when the minimum liquidity requirement is breached, or when significant changes in cash balance occur. This real-time warning system enables lenders to manage potential risks and improve their overall risk management strategy.

Upgrade Your DACA Process

If you’re a lender tired of outdated, slow, and costly risk management processes, we want to help.

To learn more and sign up, visit Arc for Lenders.